What is Health Insurance Pooling? Understanding Financial Risk & Costs

- Sydney Little

- Feb 16

- 6 min read

For many organizations, health insurance is still treated as a line-item expense. In simple terms, it’s something negotiated once a year and absorbed into operating costs. In reality, health insurance behaves much more like a financial risk exposure than a traditional benefit.

Executives often experience this firsthand at renewal. Even after maintaining stable headcount, managing claims responsibly, and making thoughtful plan design choices, costs can rise sharply. A single year of unfavorable claims can trigger double-digit increases, disrupting budgets and long-term forecasts. From a financial perspective, this volatility makes health insurance less predictable than most other operating expenses.

The common misconception is that plan design alone controls costs. Think higher deductibles, narrower networks, or shifting contributions. While these levers influence employee behavior, they do not address the core issue: how risk is distributed. Health insurance costs fluctuate primarily because medical risk is uneven and unpredictable at the individual level.

This is where health insurance pooling enters the conversation as a risk-management mechanism. Pooling determines how much financial exposure an organization retains versus how much is shared across a broader group. For executives, this distinction matters because it directly affects forecasting accuracy, cost stability, and long-term financial planning.

Table of Contents

The Risk-Sharing System Behind Every Health Plan

How Health Insurance Pooling Stabilizes Costs (When It Works)

When Pooling Helps — and When It Doesn’t

The Pooling Options Executives Actually Encounter

Key Takeaways

Point | Details |

Health Insurance Is a Financial Risk, Not a Fixed Expense | Health insurance costs behave like a volatility exposure on the balance sheet, not a predictable operating cost. Annual swings are driven more by risk concentration than plan design. |

All Health Plans Rely on Risk Pooling | Every health plan involves pooling. The strategic difference lies in who shares risk, how broadly it is distributed, and how much exposure remains with the organization. |

Smaller Groups Experience Greater Cost Volatility | Limited participation magnifies the financial impact of high-cost claims, making renewals more sensitive to individual events rather than overall utilization trends. |

Pooling Stabilizes Costs by Reducing Variance | Effective health insurance pooling spreads high-cost claims across a larger base, converting catastrophic outliers into manageable fluctuations over time. |

Pooling Trades Upside for Predictability | Pooled arrangements are not guarantees of lower costs. They reduce volatility and improve forecasting at the expense of capturing short-term savings from favorable claims experience. |

Plan Structure Determines Risk Ownership | Fully insured, level-funded, PEO-based, and self-funded models differ primarily in who owns claims risk, how predictable costs are, and what governance responsibilities leadership retains. |

Pooling Is a Strategic Decision | Choosing a pooling approach is a financial and governance decision that affects budgeting accuracy, long-term planning, and leadership oversight—not just employee benefits. |

The Risk-Sharing System Behind Every Health Plan

Every health plan relies on some form of insurance pooling. The difference between plans is not whether pooling exists, but who participates in the pool and who ultimately absorbs the risk.

At a basic level, pooling spreads healthcare costs across multiple participants so that no single individual bears the full financial impact of serious medical events. Group health insurance pooling applies this concept across an employer population, allowing costs to be shared rather than isolated.

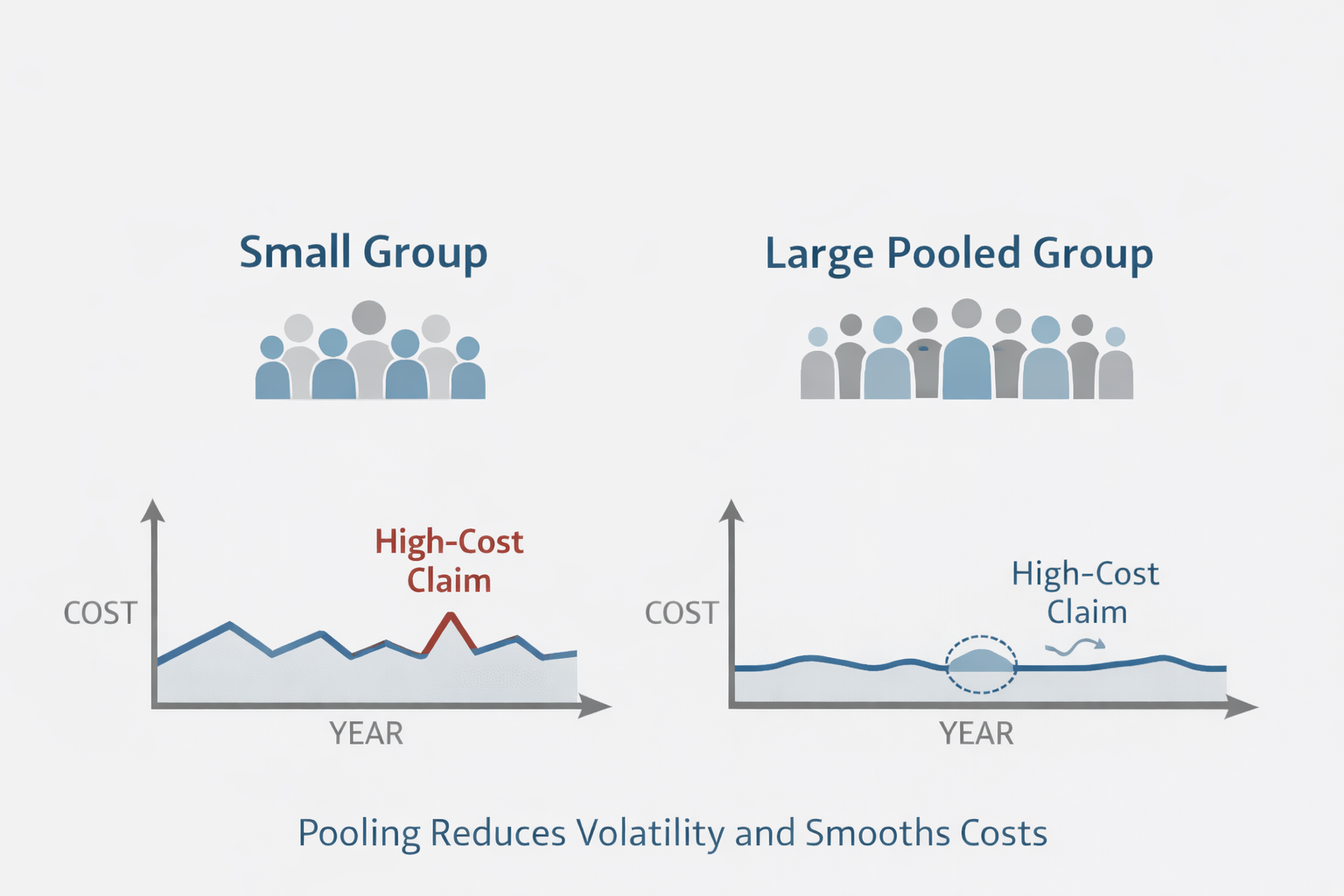

Scale matters. In smaller organizations, individual claims carry greater weight. One significant diagnosis or hospitalization can distort total healthcare spending for the entire group. Larger pools dilute this effect by distributing costs across more participants, creating greater stability.

An executive way to think about pooling is this: it is the difference between shared liability and retained exposure. Smaller pools resemble individual risk. Larger pools behave more like an averaged financial system. Understanding this distinction shifts the conversation away from benefits preference and toward risk allocation.

How Health Insurance Pooling Stabilizes Costs (When It Works)

When health insurance pooling works as intended, it stabilizes costs by reducing variance. High-cost claims still occur, but their financial impact is absorbed across a broader base rather than concentrated within a single organization.

Consider a simple example. In a group of 20 to 30 employees, a single six-figure medical claim can materially affect annual costs. In a pool of several thousand lives, that same claim becomes manageable. The expense exists, but it no longer destabilizes the system.

This is the primary benefit of health insurance pooling. By spreading risk across a larger and more diverse population, healthcare cost sharing converts unpredictable outliers into manageable fluctuations. Participation and demographic diversity are critical. When too few participants carry disproportionate risk, pooling loses effectiveness.

For leadership teams asking how health insurance pooling works, the answer is largely mathematical. Larger, balanced pools produce smoother financial outcomes. Smaller or fragmented pools produce volatility. This is what cost smoothing looks like in practice.

When Pooling Helps — and When It Doesn’t

Pooling is not a universal solution, and treating it as one often leads to frustration. Its value depends on organizational priorities and risk tolerance.Pooling tends to benefit organizations that prioritize predictability over optimization. Leaders who value steadier renewals and fewer extreme swings often find pooled arrangements attractive. Larger or more diverse workforces also benefit because risk naturally balances over time.

However, pooling can be less satisfying for organizations expecting direct rewards for favorable claims experience. In pooled environments, strong performance does not always translate into immediate savings. Upside is shared just as risk is shared.

Nonprofits and care-focused organizations frequently operate in a gray zone. Their missions require competitive benefits, while workforce demographics can increase claims variability. For these groups, pooling may offer stability, but not insulation from broader market forces.

The key trade-off is straightforward: pooling reduces volatility but limits upside. It is not a guarantee of lower costs. It is a strategic choice about how much financial uncertainty leadership is willing to accept

5. The Pooling Options Executives Actually Encounter

In practice, executives are not choosing between abstract pooling models. They are choosing between structures that define control, exposure, and predictability.

Most organizations evaluate some combination of:

Fully insured group plans, which transfer most claims risk to an insurer in exchange for predictable premiums.

Level-funded or partially pooled plans, which blend predictable monthly costs with limited claims exposure.

PEO or association-based pools, which leverage larger groups to stabilize costs while reducing plan-level control.

Self-funded plans with stop-loss coverage, which increase retained risk in exchange for transparency and potential savings.

Each option answers the same questions differently:

Who ultimately owns claims risk?

How predictable are annual costs?

What governance and oversight responsibilities remain with leadership?

Viewing these options through the lens of health insurance pooling and healthcare cost sharing helps align benefits strategy with financial objectives. This is not merely a benefits decision. It is a governance decision that affects forecasting, oversight, and long-term sustainability.

Frequently Asked Questions

How does health insurance pooling work? Pooling works by absorbing individual medical claims into a collective group. Instead of one organization bearing the full impact of a costly claim, expenses are distributed across the pool, reducing volatility and smoothing year-to-year costs.

Why do smaller organizations feel cost increases more sharply? Smaller groups have less risk diversification. A single high-cost claim can materially affect total healthcare spending, leading to larger renewal increases compared to larger, more diverse pools.

Does pooling always lower healthcare costs? No. Pooling is designed to reduce volatility, not guarantee lower costs. It trades the potential upside of favorable claims experience for greater predictability and stability over time.

What types of plans use health insurance pooling? Fully insured plans, level-funded plans, PEO and association-based plans all rely on pooling to some degree. The key difference is how much risk remains with the employer versus being shared or transferred.

Is pooling the same as self-funding? No. Self-funded plans retain more claims risk at the employer level, typically with stop-loss protection. Pooling shares risk across a broader group, reducing exposure but also limiting upside.

How should leadership evaluate pooling options? Executives should assess risk tolerance, cost predictability needs, workforce size, and governance preferences. Pooling decisions should align with financial planning and long-term organizational strategy.

Recommended

Comments